What can you do, when your HDB reached 5 Years MOP?

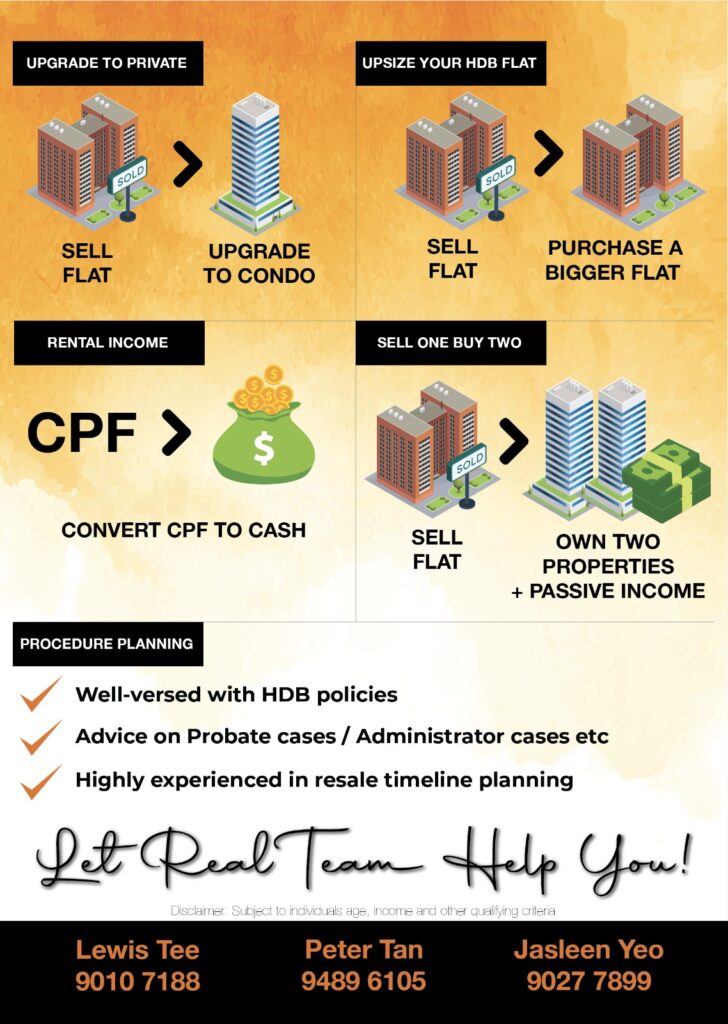

What Are The Available Options When Your HDB Reached MOP? (Agent) Lewis: Mr. and Mrs. Soh, Thank you for your time. I understood, your current flat has reached the HDB MOP period. Any plan...

Navis Living Group

What Are The Available Options When Your HDB Reached MOP? (Agent) Lewis: Mr. and Mrs. Soh, Thank you for your time. I understood, your current flat has reached the HDB MOP period. Any plan...

The article shared the key consideration, mainly from the investment point of view. How to go about managing HDB and private condo. Making you as a property investor with lower possible non-property related payment

4 Questions To Ask Before Upgrading Your HDB You have been staying in your newly BTO HDB Flat for almost five years. Your neighbor has been talking about upgrading to a bigger flat, upgrading...