2022 Q2 – Market Outlook

The property market has been moving rapidly. Read about what happened over the last Quarter and what to expect, from my view

Navis Living Group

The property market has been moving rapidly. Read about what happened over the last Quarter and what to expect, from my view

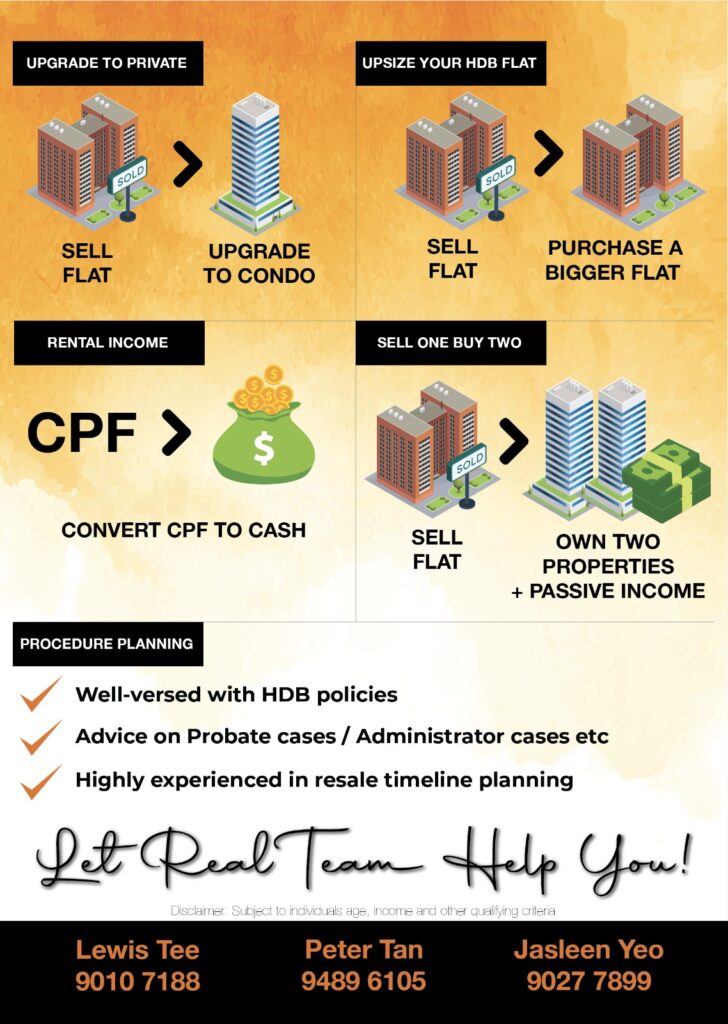

What Are The Available Options When Your HDB Reached MOP? (Agent) Lewis: Mr. and Mrs. Soh, Thank you for your time. I understood, your current flat has reached the HDB MOP period. Any plan...

Have you heard about the recent new launch in district 14, Singapore? Yes, it is Penrose. This has been a hot topic discussed by many buyers looking for new launches and also, real estate...

Sharing of the market of 2020. With the current Coronavirus situation. How was the market moving and what is the projection basing on experience and background

Covid-19 has been going on for some time, and nobody knows when it will end, or a vaccine will be ready. However, we can’t wait for this pandemic to end totally before deciding to...

Being a professional Property Wealth Planner (PWP), many people turn to me, asking me a magic question.“Which property should I invest? So I can make money”.Jokingly, I will reply,“If I am so accurate, I...

With many companies undergoing globalization, many Singapore citizens are traveling out of Singapore. Likewise, many foreign talents have also traveled into Singapore to work due to the skill set requirements. With the movement of...

很多时候, 我们都会听到人家在说。 危机就是商机, 有了商机就有利润。 可是, 我们怎么就没有遇见好的商机呢。 原因很简单。 我们习惯了稳扎稳打。 可是, 投资回报可不是稳扎稳打的。 危机跟回报是相对的。 危险性高, 回报利润就高。以一个投资者,我们能够做的就是风险维持在我们可以控制范围里面。 投资选项 股市 在市场上, 比较普片的投资就属股票, 黄金和房地产了。以我个人分析, 在三个投资选择里, 股票投资通常被称为“高风险”。 投资股票的主要风险是可能导致资本损失。 股票的走向, 也是您无法控制的。 比方, 突发事件或公司内部的不利发展, 很可能会严重影响股价和您的投资组合的价值。 黄金 对于黄金投资, 尽管黄金与股市有反比关系,但股票市场也与黄金有着深远的联系。 在股市严重下滑的情况下,投资者通常将黄金视为避风港。 据推测,当我们遇到全球市场下跌时,股票和货币就会下跌。 一些投资变得不那么理想,投资者认为黄金会给他们提供喘息的空间。 但是,这并非总是如此,投资者可能会被烧死。 房地产...

Crisis For most of us, investment is usually the lowest priority when we are experiencing an extraordinary global crisis, as we are unsure of the current situation. The most common concern is, if I...

Since 1960, HDB was formed to provide public housing. Over the years, it has played a huge part in providing majority of the Singapore citizens with a roof over their heads. To date, there...