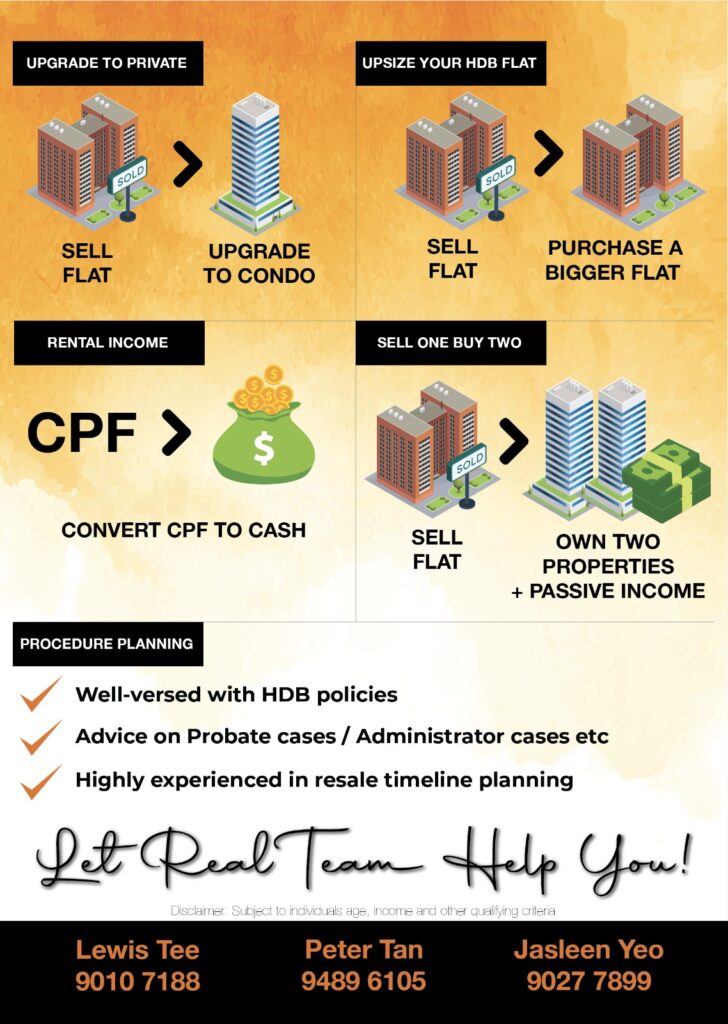

Market Outlook – Q2 2020

Sharing of the market of 2020. With the current Coronavirus situation. How was the market moving and what is the projection basing on experience and background

Navis Living Group

Sharing of the market of 2020. With the current Coronavirus situation. How was the market moving and what is the projection basing on experience and background

很多时候, 我们都会听到人家在说。 危机就是商机, 有了商机就有利润。 可是, 我们怎么就没有遇见好的商机呢。 原因很简单。 我们习惯了稳扎稳打。 可是, 投资回报可不是稳扎稳打的。 危机跟回报是相对的。 危险性高, 回报利润就高。以一个投资者,我们能够做的就是风险维持在我们可以控制范围里面。 投资选项 股市 在市场上, 比较普片的投资就属股票, 黄金和房地产了。以我个人分析, 在三个投资选择里, 股票投资通常被称为“高风险”。 投资股票的主要风险是可能导致资本损失。 股票的走向, 也是您无法控制的。 比方, 突发事件或公司内部的不利发展, 很可能会严重影响股价和您的投资组合的价值。 黄金 对于黄金投资, 尽管黄金与股市有反比关系,但股票市场也与黄金有着深远的联系。 在股市严重下滑的情况下,投资者通常将黄金视为避风港。 据推测,当我们遇到全球市场下跌时,股票和货币就会下跌。 一些投资变得不那么理想,投资者认为黄金会给他们提供喘息的空间。 但是,这并非总是如此,投资者可能会被烧死。 房地产...

Crisis For most of us, investment is usually the lowest priority when we are experiencing an extraordinary global crisis, as we are unsure of the current situation. The most common concern is, if I...

What has CPF Accrued Interest affected the sales proceed. How can property owner do, to keep the accrued interest low.

Who Should Do Mortgage Refinancing? For many Singaporeans, the flat we purchase usually does not belong to us for several years, the reason behind that being that we put our purchased flat on a...

Got this WhatsApp during one of the afternoons. My mind was running actively, running through my list of contact that was named Frank. Lucky, I have only 1 friend who’s name is Frank. Quickly,...