What can you do, when your HDB reached 5 Years MOP?

What Are The Available Options When Your HDB Reached MOP? (Agent) Lewis: Mr. and Mrs. Soh, Thank you for your time. I understood, your current flat has reached the HDB MOP period. Any plan...

Navis Living Group

What Are The Available Options When Your HDB Reached MOP? (Agent) Lewis: Mr. and Mrs. Soh, Thank you for your time. I understood, your current flat has reached the HDB MOP period. Any plan...

Sharing of the market of 2020. With the current Coronavirus situation. How was the market moving and what is the projection basing on experience and background

What has CPF Accrued Interest affected the sales proceed. How can property owner do, to keep the accrued interest low.

Who Should Do Mortgage Refinancing? For many Singaporeans, the flat we purchase usually does not belong to us for several years, the reason behind that being that we put our purchased flat on a...

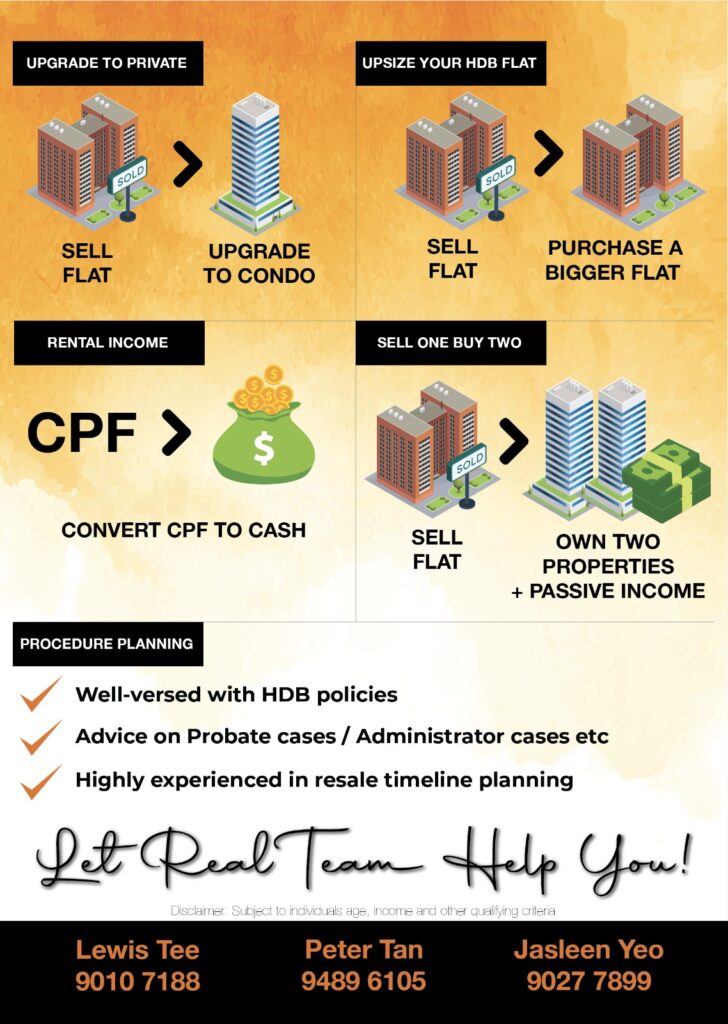

The article shared the key consideration, mainly from the investment point of view. How to go about managing HDB and private condo. Making you as a property investor with lower possible non-property related payment

Should The First Home You Are Getting Be HDB BTO Flat Congratulation, when you start to reach about this post, it tells that, you are about to make one of the bigger ticket investment...

4 Questions To Ask Before Upgrading Your HDB You have been staying in your newly BTO HDB Flat for almost five years. Your neighbor has been talking about upgrading to a bigger flat, upgrading...