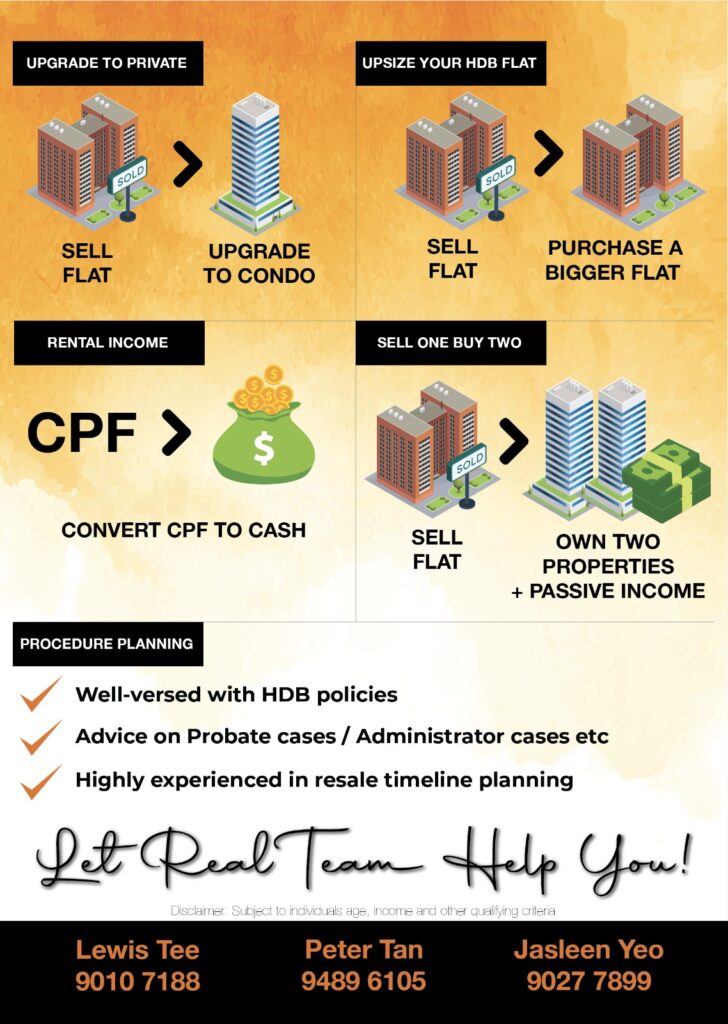

What can you do, when your HDB reached 5 Years MOP?

What Are The Available Options When Your HDB Reached MOP? (Agent) Lewis: Mr. and Mrs. Soh, Thank you for your time. I understood, your current flat has reached the HDB MOP period. Any plan...

Navis Living Group

What Are The Available Options When Your HDB Reached MOP? (Agent) Lewis: Mr. and Mrs. Soh, Thank you for your time. I understood, your current flat has reached the HDB MOP period. Any plan...

Sharing of the market of 2020. With the current Coronavirus situation. How was the market moving and what is the projection basing on experience and background

With many companies undergoing globalization, many Singapore citizens are traveling out of Singapore. Likewise, many foreign talents have also traveled into Singapore to work due to the skill set requirements. With the movement of...

Since 1960, HDB was formed to provide public housing. Over the years, it has played a huge part in providing majority of the Singapore citizens with a roof over their heads. To date, there...

What has CPF Accrued Interest affected the sales proceed. How can property owner do, to keep the accrued interest low.

Who Should Do Mortgage Refinancing? For many Singaporeans, the flat we purchase usually does not belong to us for several years, the reason behind that being that we put our purchased flat on a...

The article shared the key consideration, mainly from the investment point of view. How to go about managing HDB and private condo. Making you as a property investor with lower possible non-property related payment

Why You Should Buy A HDB Resales As Your First Property? Getting married is one of the major milestones in life. During that process, you have thousand and zillion things to worry and get...

The article share, some of the basic consideration before you start sourcing for your HDB flat. Is not the must-do list but more the recommendation

4 Questions To Ask Before Upgrading Your HDB You have been staying in your newly BTO HDB Flat for almost five years. Your neighbor has been talking about upgrading to a bigger flat, upgrading...